The U.S. housing market is facing increased scrutiny in 2025, with buyers, sellers, and investors all asking the same urgent question: Is a housing crash coming? The uncertainty fueled by rising mortgage rates, inflation concerns, and economic fluctuations has triggered anxiety reminiscent of the 2008 financial crisis. However, by examining current housing market trends, economic indicators, and expert forecasts, we can draw a clearer distinction between myths and reality. Not every market slowdown is a crash and not every price drop signals a bubble burst.

U.S. Housing Market Overview Chart (2020–2024)

What Is a Housing Crash, Really?

A real estate market crash involves a dramatic drop in home values, usually triggered by excessive speculation, unaffordable lending practices, and a sudden increase in supply due to foreclosures or distress sales. For reference, during the 2008 crisis, home prices fell by over 30% in some regions and took years to recover.

In contrast, today’s market is fundamentally different. Key metrics, such as inventory levels, buyer qualifications, and construction activity, tell a much less alarming story.

Myth 1: Home Prices Are Headed for a Major Collapse

The truth: While some overheated markets may see price corrections, a nationwide collapse is not expected.

According to the National Association of Realtors (NAR), home prices rose modestly in early 2025 and are projected to remain steady or grow slightly in most regions this year. Tight inventory is one of the biggest reasons. NAR 2025 Forecast

Meanwhile, Fannie Mae predicts a balanced outlook: slower growth but continued resilience in key markets with strong employment and population growth. Fannie Mae Housing Forecast May 2025

This suggests that we are not seeing a housing bubble burst but rather a market correction from the unsustainable growth experienced during the pandemic.

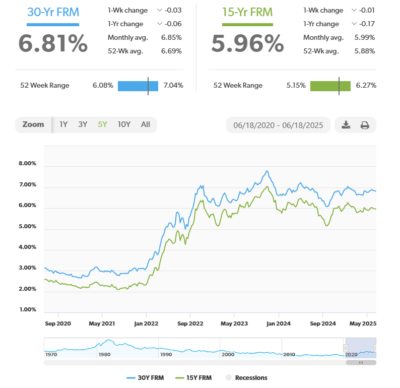

Myth 2: High Mortgage Rates Will Crash the Market

30-Year Mortgage Rate Trends Chart (2020–2025)

The reality: Higher mortgage rates reduce affordability, but they also prevent a flood of listings.

After the Federal Reserve’s rate hikes in 2022–2024, mortgage rates climbed to over 7%, causing a slowdown in sales. However, many homeowners who locked in ultra-low rates during 2020–2021 are staying put, leading to a “lock-in effect” that keeps inventory low. Freddie Mac’s Mortgage Rate Data

This limited supply continues to support home prices. As Redfin reports, while buyer demand is softer, motivated and financially qualified buyers are still active in many areas. Redfin Housing Market Tracker

Myth 3: We’re in a New Housing Bubble

Comparison table of lending standards, foreclosure rates, and supply between the 2010 and 2025

Some analysts compare today’s market to the early 2000s, raising concerns about a housing bubble. But key fundamentals suggest otherwise.

-

Lending standards today are far more rigorous due to post-2008 regulations such as the Dodd-Frank Act.

-

Most buyers are purchasing homes they intend to live in, not flip.

-

Investor activity has decreased significantly in 2025, reducing speculative pressure on prices.

-

There is still a housing shortage: According to Realtor.com, the U.S. is short by over 4 million housing units.

These conditions indicate a supply-driven affordability crisis, not a bubble inflated by speculation.

Expert Outlook: What’s Next for the Housing Market?

Here’s what leading analysts and financial institutions predict for the remainder of 2025:

-

Goldman Sachs has shifted its stance to a soft landing scenario, suggesting that home prices may stabilize or decline slightly in select high-cost markets, but no crash is forecasted. Goldman Sachs U.S. Housing Outlook

-

Zillow expects modest price gains of 1–3% nationally, driven by low inventory and sustained demand in metro regions with strong labor markets. Zillow Home Value Forecast

-

CoreLogic reports that foreclosure rates remain historically low, another strong sign of market health. CoreLogic Housing Insights

These expert sources agree: the market is slowing, but not crashing.

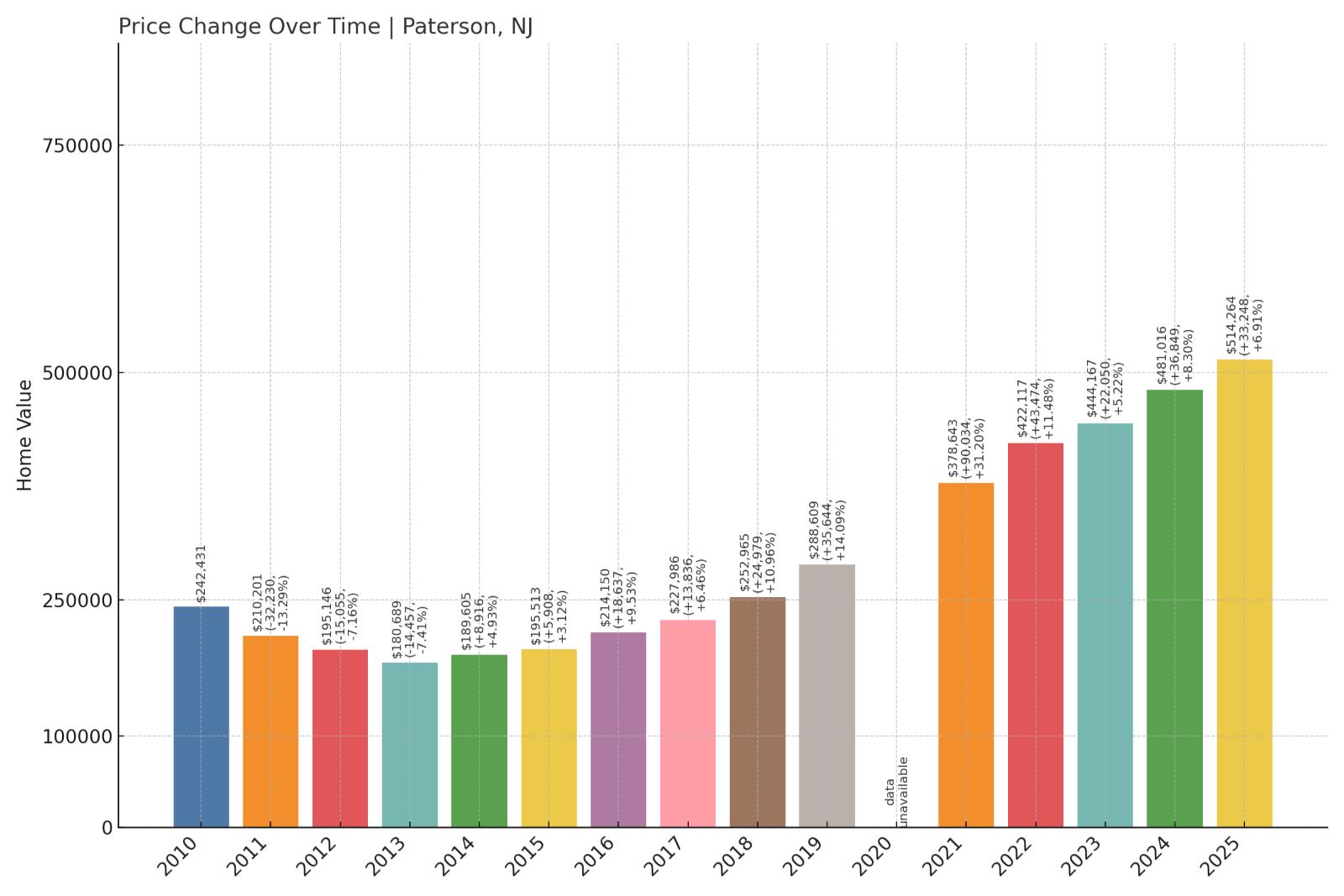

Regional Variations Matter

U.S. map highlighting states with rising and falling home prices in 2025

While the national outlook is stable, local housing markets vary widely. Areas that saw the fastest price increases during the pandemic such as parts of California, Nevada, and Texas are more likely to experience price adjustments. In contrast, suburban and mid-sized markets with limited new construction may remain competitive.

If you’re in a market like Morris County, NJ, for example, where inventory remains low and demand steady, you’re more likely to see stability or moderate appreciation rather than a drop.

What This Means for Buyers and Sellers

Buyers:

Now may be a good time to re-enter the market, especially if you’re looking to avoid bidding wars. You may also be able to negotiate better terms or seller concessions. However, don’t expect steep discounts or a flood of distressed listings.

Sellers:

If you price your home appropriately and prepare it for sale, it can still sell quickly especially in high-demand neighborhoods. While you may not see the rapid appreciation of 2021, pricing strategy and marketing are now more important than ever.

Final Thoughts: No Crash, Just a Market Reset

In short, the housing market in 2025 is not crashing it is recalibrating. The extreme conditions of the pandemic years are behind us, and the current landscape reflects a transition to a more balanced and sustainable market.

Staying informed, relying on credible data, and working with experienced real estate professionals will help you make the best decisions in this evolving environment. lets connect for more insights