Understanding ARMs With Jackie Scura in Morris County

Residential homes in Morris County with adjustable-rate mortgage planning

For homebuyers in Morris County, navigating mortgage options can feel overwhelming, especially when adjustable-rate mortgages (ARMs) enter the discussion. Jackie Scura frequently works with buyers who are unsure about ARMs because of long-standing myths, partial explanations, or outdated information passed through word of mouth.

This is why having ARMs explained clearly and accurately is essential before making a major financial decision in Morris County’s competitive housing market. ARMs are not unpredictable or unstable products. They are structured loans with defined rules, protections, and adjustment mechanisms designed to respond to changing market conditions.

Instead of relying on assumptions, it’s important to understand how these loans actually work. Below are 10 ARM myths homebuyers in Morris County should know—along with detailed explanations that clarify the truth behind each one.

1. ARMs Are Too Risky for Homebuyers

Homebuyers learning about ARM mortgage protections

One of the most common concerns Jackie Scura hears in Morris County is that ARMs are inherently risky. This belief usually comes from misunderstanding how the loan is structured.

In reality, ARMs include built-in safeguards such as rate caps, which limit how much your interest rate can increase during each adjustment period and over the life of the loan. These protections ensure that even if market rates rise significantly, your mortgage payments remain within a controlled and predictable range. Risk exists in any loan—but ARMs are designed to manage it, not amplify it.

2. Interest Rates Only Go Up

Mortgage interest rate trends for adjustable rate mortgages

Many buyers assume ARMs only move in one direction: upward. This misconception often discourages Morris County homebuyers from even considering them.

However, ARMs are tied to financial indexes that fluctuate with broader economic conditions. If those indexes decrease, your interest rate can also go down. This means borrowers can benefit from lower payments in favorable market environments—something fixed-rate mortgages do not offer.

3. Monthly Payments Are Unpredictable

Homeowner budgeting ARM mortgage payments

Another major myth is that ARM payments become unpredictable after the fixed period ends.

Jackie Scura explains that ARM adjustments follow a clearly defined structure based on three key components: the index rate, lender margin, and adjustment caps. While payments may change, they do so within strict contractual limits. This structure allows homeowners in Morris County to anticipate potential changes and plan accordingly.

4. ARMs Are Only for Short-Term Homeowners

Long-term homeowners using adjustable rate mortgages

It is often believed that ARMs only make sense for buyers who plan to move within a few years. While short-term homeowners can benefit, this is not the only use case.

In Morris County, some long-term buyers choose ARMs strategically when they expect income growth, plan to refinance, or want to allocate savings from lower initial payments toward investments or renovations. When ARMs are explained fully, their flexibility becomes a key advantage rather than a limitation.

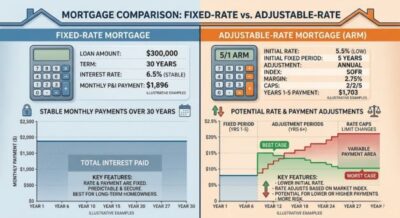

5. Fixed-Rate Mortgages Are Always Better

Comparing fixed rate and adjustable rate mortgages

Fixed-rate mortgages are popular in Morris County due to their stability, but that does not automatically make them the better financial option.

ARMs often start with lower introductory interest rates, which can significantly reduce monthly payments in the early years of homeownership. Jackie Scura emphasizes that this early savings can be strategically used to build equity faster, invest elsewhere, or improve financial flexibility.

6. ARMs Caused the Housing Crisis

Modern mortgage lending standards for ARMs

This is one of the most persistent misconceptions in real estate.

The 2008 financial crisis was caused by a combination of irresponsible lending practices, weak underwriting standards, and high-risk mortgage products—not ARMs alone. Modern ARMs are heavily regulated, transparent, and include safeguards that were not consistently enforced in the past.

7. You Can’t Plan for Future Payment Changes

Financial planning for adjustable rate mortgage payments

Some Morris County buyers avoid ARMs because they believe future payments are impossible to estimate.

In reality, ARMs are tied to publicly available financial indexes and include clear adjustment schedules and rate caps. While exact future payments are not fixed, borrowers can model potential scenarios and make informed financial plans based on defined boundaries.

8. ARMs Are Too Complicated to Understand

Mortgage advisor explaining ARM loan structure

Many assume ARMs are overly complex and difficult to interpret.

Jackie Scura simplifies them into two phases: a fixed-rate period, followed by a variable adjustment period tied to a benchmark index. Once broken down this way, ARMs are often easier to understand than many traditional loan structures, especially for first-time buyers in Morris County.

9. You Will Always Pay More With an ARM

Potential savings with adjustable rate mortgages

Another misconception is that ARMs inevitably cost more than fixed-rate loans over time.

The reality depends on interest rate trends and how long the loan is held. In many cases, especially when rates remain stable or decline, ARMs can result in lower total interest paid over the life of the loan. This makes them a potentially cost-effective option in certain market conditions.

10. ARMs Don’t Make Sense in Today’s Morris County Market

Modern homebuyers in Morris County using ARM mortgages

Some buyers believe ARMs are outdated or irrelevant in modern lending environments.

However, ARMs remain widely used in Morris County and across the country. In fluctuating interest rate environments, they can offer valuable flexibility that fixed-rate mortgages cannot. Jackie Scura notes that when aligned with a borrower’s financial strategy, ARMs can be a powerful tool rather than a risky alternative.

Final Thoughts From Jackie Scura for Morris County Buyers

For homebuyers in Morris County, the challenge is rarely the mortgage itself—it is the misinformation surrounding it. Once ARMs are explained clearly and in full context, they become a legitimate financing option rather than something to avoid.

For many buyers, ARMs may offer:

- Lower initial monthly payments

- Structured protections through rate caps

- Financial flexibility for changing life goals

- Potential long-term savings depending on market conditions

Ultimately, the best mortgage is not about perception—it is about alignment with your financial strategy and the realities of the Morris County housing market.